Hi, I want to calculate monthly payment for a loan that has promotional interest rate 0% for part of the loan.

I believe that I have result, but I would like to confirm, that my approach is correct.

What I have:

loan amount is 10000

i (promotional 1-6M)=0%

i (standard 7-12M)=1,606% p.m.

n =12

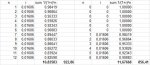

What I did - I took annuity formula and put it to Excel to find payment (see the print screen).

First columns are equivalent of pmt function in Excel (to confirm that calculation is OK). Second is the result with promotional rate.

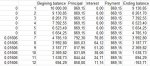

I tried another way - amortization table and then by macro and bisection method found the payment that gives 0 for balanace at the end of the period. This gives same result as here 856,41

What I am not sure about:

- why to apply power of 1 to 6 for second half of the year? Why not 7 to 12, it is in fact 7th period. Do I understand it as first period with applied interest?

- is there "single" formula for this? Something like "pmt" in Excel?

Thank you.

I believe that I have result, but I would like to confirm, that my approach is correct.

What I have:

loan amount is 10000

i (promotional 1-6M)=0%

i (standard 7-12M)=1,606% p.m.

n =12

What I did - I took annuity formula and put it to Excel to find payment (see the print screen).

First columns are equivalent of pmt function in Excel (to confirm that calculation is OK). Second is the result with promotional rate.

I tried another way - amortization table and then by macro and bisection method found the payment that gives 0 for balanace at the end of the period. This gives same result as here 856,41

What I am not sure about:

- why to apply power of 1 to 6 for second half of the year? Why not 7 to 12, it is in fact 7th period. Do I understand it as first period with applied interest?

- is there "single" formula for this? Something like "pmt" in Excel?

Thank you.