Problem Description:

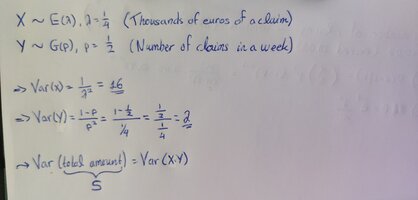

The size X (in thousands of euros) of a compensation paid by an insurance company has the exponential distribution with parameter λ=1/4.

The number of claims paid by the insurance company over a week has a geometric distribution with parameter p=1/2.

How much is the variance of the (total) amount of claims paid by the insurance company over a week?

Solution: 64

Can someone help me with the methodology I should follow in order to reach a solution in this problem? Thank you in advance!

The size X (in thousands of euros) of a compensation paid by an insurance company has the exponential distribution with parameter λ=1/4.

The number of claims paid by the insurance company over a week has a geometric distribution with parameter p=1/2.

How much is the variance of the (total) amount of claims paid by the insurance company over a week?

Solution: 64

Can someone help me with the methodology I should follow in order to reach a solution in this problem? Thank you in advance!