Dear all,

Im trying to calculate the Max purchase a customer can afford.

where (cash) downpayment +(tax 1) +(tax 2) = 1,809,000

where purchase price - loan = downpayment (cash + tax 1 + tax2 + fix processing fee ) = 1,809,000

In this case i assume tax 2 =0%

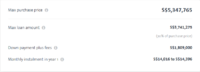

1) Max Purchase Price: *I can't figure out*

2) Loan: Using Loan Available (Assuming $3,741,275)

3) Deposit= Using Cash Available (Assuming $1,809,000)

4) Tax 1: 4% of Purchase Price (with the condition as below)

5) Tax 2: 0% of Purchase Price*

6) Processing Fee: Fix at $4,000

Is there a solution to:

Loan (2) + Deposit/ Cash(3) + tax 1(4) + tax 2(5) + Processing Fee(6) = Max Purchase Price(1)

Finding out my maximum possible Purchase price based on my Available Cash and LOAN

Tax 1 and Tax 2 is depending on Purchase Price

For tax 1, there is some conditions:*

If Purchase Price = $0, Tax 1 is 0%*

If Purchase Price <= $180,000, Tax 1 is 1%*

If Purchase Price <= $360,000, Tax 1 is 2%*

If Purchase Price <= $1,000,000, Tax 1 is 3%

Else 4%

If tax 1 is 3%, tax 1 will be 3%-$5400

If tax 1 is 4%, tax 1 will be 4%-$15400

Please take the answer from the reference.

Im trying to calculate the Max purchase a customer can afford.

where (cash) downpayment +(tax 1) +(tax 2) = 1,809,000

where purchase price - loan = downpayment (cash + tax 1 + tax2 + fix processing fee ) = 1,809,000

In this case i assume tax 2 =0%

1) Max Purchase Price: *I can't figure out*

2) Loan: Using Loan Available (Assuming $3,741,275)

3) Deposit= Using Cash Available (Assuming $1,809,000)

4) Tax 1: 4% of Purchase Price (with the condition as below)

5) Tax 2: 0% of Purchase Price*

6) Processing Fee: Fix at $4,000

Is there a solution to:

Loan (2) + Deposit/ Cash(3) + tax 1(4) + tax 2(5) + Processing Fee(6) = Max Purchase Price(1)

Finding out my maximum possible Purchase price based on my Available Cash and LOAN

Tax 1 and Tax 2 is depending on Purchase Price

For tax 1, there is some conditions:*

If Purchase Price = $0, Tax 1 is 0%*

If Purchase Price <= $180,000, Tax 1 is 1%*

If Purchase Price <= $360,000, Tax 1 is 2%*

If Purchase Price <= $1,000,000, Tax 1 is 3%

Else 4%

If tax 1 is 3%, tax 1 will be 3%-$5400

If tax 1 is 4%, tax 1 will be 4%-$15400

Please take the answer from the reference.