2010reinhm

New member

- Joined

- Oct 8, 2015

- Messages

- 1

struggling big time with this assignment.

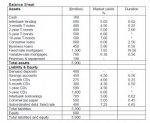

i need to put the assets and liabilities into their different time bands (buckets).

however, the balance sheet provided does not provide repricing information for consumer loans or business loans? is there a way to figure out when these loans are repriced?

the following notes are provided for the balance sheet (no information for consumer or business loan repricing though?)

1. The coupon rate paid on 5-year T-bonds is 5.00% (per annum). The coupon

payment is received bi-annually.

2. The coupon rate paid on 10-year T-bonds is 6.00% (per annum) and the

coupon payment is received annually.

3. Variable rate mortgages are repriced at every six months.

4. 1-year CDs have been issued with a coupon rate of 4.00% (per annum, biannual

payments)

5. 5 year CDs has been issued with a coupon rate of 5.00% (per annum, annual

payments).

6. The current price on IRFs is $98.75 per $100 FV with a contract size of

$1,000,000.The duration of the deliverable security is xxx yrs. The sensitivity

of the futures and spot rates (b ratio) is assumed to be expressed in the

regression ∆Sp = -2.5 + 1.15∆Fp.

7. We further note that the 12-month cumulative Lgap is forecast to rise and that

our loan base is expanding at a rate faster than our deposits.

8. xxx denotes missing data that will be provided in tute classes.

I would extremely grateful for any help at all

i need to put the assets and liabilities into their different time bands (buckets).

however, the balance sheet provided does not provide repricing information for consumer loans or business loans? is there a way to figure out when these loans are repriced?

the following notes are provided for the balance sheet (no information for consumer or business loan repricing though?)

1. The coupon rate paid on 5-year T-bonds is 5.00% (per annum). The coupon

payment is received bi-annually.

2. The coupon rate paid on 10-year T-bonds is 6.00% (per annum) and the

coupon payment is received annually.

3. Variable rate mortgages are repriced at every six months.

4. 1-year CDs have been issued with a coupon rate of 4.00% (per annum, biannual

payments)

5. 5 year CDs has been issued with a coupon rate of 5.00% (per annum, annual

payments).

6. The current price on IRFs is $98.75 per $100 FV with a contract size of

$1,000,000.The duration of the deliverable security is xxx yrs. The sensitivity

of the futures and spot rates (b ratio) is assumed to be expressed in the

regression ∆Sp = -2.5 + 1.15∆Fp.

7. We further note that the 12-month cumulative Lgap is forecast to rise and that

our loan base is expanding at a rate faster than our deposits.

8. xxx denotes missing data that will be provided in tute classes.

I would extremely grateful for any help at all