yrstrulysa

New member

- Joined

- Aug 28, 2022

- Messages

- 3

I have this policy below, and i would like to calculated (non)-eligible litres:

How do i get the amount in Non-elible Litres a seen in screen shot and am i correct to say that 80% is the percentage used to get eligible litres?

POLICY a) The general fuel levy increases by 16.0c per litre and the Road Accident Fund (RAF) levy by 9.0c per litre respectively, with effect from 01 April 2020, as follows: i) General Fuel levy = Increases from 339.0 c/l to 355.0 c/l; and ii) RAF levy = Increases from 198.0 c/l to 207.0 c/l. b) The diesel refund in respect of on-land primary sector beneficiaries is 40% of the general fuel levy of 355.0 c/l, which equals 142.0 c/l of the qualifying 80% of diesel consumption. c) As from 1 April 2016, the diesel refund levy on the generation of electricity by Eskom’s open cycle gas turbines was reduced to 50% of the general fuel levy.

USAGE TYPES PREVIOUS NEW On Land (Farming, Mining & Forestry) 333.6 c/l 349.0 c/l Offshore (Commercial fishing, Coastwise Shipping, Offshore Mining & NSRI) 537.0 c/l 562.0 c/l Electricity Generation Plants 367.5 c/l 384.5 c/l Rail & Harbour Services 198.0 c/l 207.0 c/l d) Where the implementation date of the new rates for RAF levy and fuel levy falls within the tax period, a factor has been determined, on which a vendor must recalculate total non-eligible and eligible litres to determine the correct litres to be entered on the VAT 201 return. e) The prescribed factor per usage type is as follows: f) The VAT vendor must recalculate total non-eligible and eligible litres purchased up to and on 31 March 2020, by using the factor (shown above) to reduce these litres to enable them to use the new rate when calculating the diesel refund. g) Examples of the calculations are shown below.

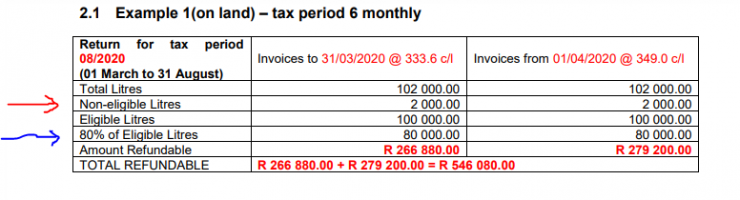

2.1 Example 1(on land) – tax period 6 monthly Return for tax period 08/2020 (01 March to 31 August) Invoices to 31/03/2020 @ 333.6 c/l Invoices from 01/04/2020 @ 349.0 c/l Total Litres 102 000.00 102 000.00 Non-eligible Litres 2 000.00 2 000.00 Eligible Litres 100 000.00 100 000.00 80% of Eligible Litres 80 000.00 80 000.00 Amount Refundable R 266 880.00 R 279 200.00 TOTAL REFUNDABLE R 266 880.00 + R 279 200.00 = R 546 080.00 On Land 0.95587 Offshore 0.95551 Electricity Generation Plants 0.95578 Rail & Harbour Services 0.9565.

) Correction of litres purchased until 31/03/2020: Total litres times factor equals recalculated litres: 102 000 litres x 0.95587 = 97 498 litres Non-eligible litres times factor equals recalculated litres: 2 000 litres x 0.95587 = 1 911 litres Recalculated eligible litres: 97 498 litres - 1 911 litres = 95 587 litres b) Return for April 2020 to be completed as follows: i) Recalculated litres plus litres purchased from 01/04/2020 equals figures for return. Total litres 97 498 (Recalculated) + 102 000 (litres from 01/04/20) = 199 498 Non-eligible litres 1 911 (Recalculated) + 2 000 (litres from 01/04/20) = 3 911 Eligible litres 95 587 (Recalculated) + 100 000 (litres from 01/04/20) = 195 587 80% of eligible litres 76 469 (Recalculated) + 80 000 (litres from 01/04/20) = 156 469 ii) Amount refundable 156 469 (litres) x 349.0 c/l = R 546 076.8

How do i get the amount in Non-elible Litres a seen in screen shot and am i correct to say that 80% is the percentage used to get eligible litres?

POLICY a) The general fuel levy increases by 16.0c per litre and the Road Accident Fund (RAF) levy by 9.0c per litre respectively, with effect from 01 April 2020, as follows: i) General Fuel levy = Increases from 339.0 c/l to 355.0 c/l; and ii) RAF levy = Increases from 198.0 c/l to 207.0 c/l. b) The diesel refund in respect of on-land primary sector beneficiaries is 40% of the general fuel levy of 355.0 c/l, which equals 142.0 c/l of the qualifying 80% of diesel consumption. c) As from 1 April 2016, the diesel refund levy on the generation of electricity by Eskom’s open cycle gas turbines was reduced to 50% of the general fuel levy.

USAGE TYPES PREVIOUS NEW On Land (Farming, Mining & Forestry) 333.6 c/l 349.0 c/l Offshore (Commercial fishing, Coastwise Shipping, Offshore Mining & NSRI) 537.0 c/l 562.0 c/l Electricity Generation Plants 367.5 c/l 384.5 c/l Rail & Harbour Services 198.0 c/l 207.0 c/l d) Where the implementation date of the new rates for RAF levy and fuel levy falls within the tax period, a factor has been determined, on which a vendor must recalculate total non-eligible and eligible litres to determine the correct litres to be entered on the VAT 201 return. e) The prescribed factor per usage type is as follows: f) The VAT vendor must recalculate total non-eligible and eligible litres purchased up to and on 31 March 2020, by using the factor (shown above) to reduce these litres to enable them to use the new rate when calculating the diesel refund. g) Examples of the calculations are shown below.

2.1 Example 1(on land) – tax period 6 monthly Return for tax period 08/2020 (01 March to 31 August) Invoices to 31/03/2020 @ 333.6 c/l Invoices from 01/04/2020 @ 349.0 c/l Total Litres 102 000.00 102 000.00 Non-eligible Litres 2 000.00 2 000.00 Eligible Litres 100 000.00 100 000.00 80% of Eligible Litres 80 000.00 80 000.00 Amount Refundable R 266 880.00 R 279 200.00 TOTAL REFUNDABLE R 266 880.00 + R 279 200.00 = R 546 080.00 On Land 0.95587 Offshore 0.95551 Electricity Generation Plants 0.95578 Rail & Harbour Services 0.9565.

) Correction of litres purchased until 31/03/2020: Total litres times factor equals recalculated litres: 102 000 litres x 0.95587 = 97 498 litres Non-eligible litres times factor equals recalculated litres: 2 000 litres x 0.95587 = 1 911 litres Recalculated eligible litres: 97 498 litres - 1 911 litres = 95 587 litres b) Return for April 2020 to be completed as follows: i) Recalculated litres plus litres purchased from 01/04/2020 equals figures for return. Total litres 97 498 (Recalculated) + 102 000 (litres from 01/04/20) = 199 498 Non-eligible litres 1 911 (Recalculated) + 2 000 (litres from 01/04/20) = 3 911 Eligible litres 95 587 (Recalculated) + 100 000 (litres from 01/04/20) = 195 587 80% of eligible litres 76 469 (Recalculated) + 80 000 (litres from 01/04/20) = 156 469 ii) Amount refundable 156 469 (litres) x 349.0 c/l = R 546 076.8