WallyMcCloud

New member

- Joined

- Mar 27, 2020

- Messages

- 3

I am trying to figure out how to calculate the effective interest according to the EU-standards (as described here: https://en.wikipedia.org/wiki/Annual_percentage_rate), in other words extract APR from that formula and use that to calculate the effective interest based on, for example:

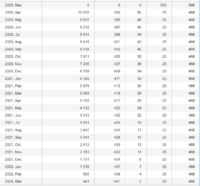

- Loan amount: 10.000

- Interest: 6%

- Period: 24 months

- Startup fee: 300

- Monthly fee: 25

According to an online calculator this should sum up to 1537 in fees and interest costs and an effective interest of 15.55%. I can't, for the love of Pythagoras, figure out how that interest is calculated! Anyone know how this is calculated?

Please note that there seems to be a difference of what is referred to as APR in this formula and what most Americans consider APR.

- Loan amount: 10.000

- Interest: 6%

- Period: 24 months

- Startup fee: 300

- Monthly fee: 25

According to an online calculator this should sum up to 1537 in fees and interest costs and an effective interest of 15.55%. I can't, for the love of Pythagoras, figure out how that interest is calculated! Anyone know how this is calculated?

Please note that there seems to be a difference of what is referred to as APR in this formula and what most Americans consider APR.

") Good work, EU! Maybe the US will catch up on this one.

Good work, EU! Maybe the US will catch up on this one.