Anonymous2019

New member

- Joined

- Sep 13, 2019

- Messages

- 3

Lately I have been studying forecasting mortality rates.

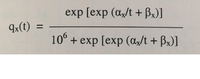

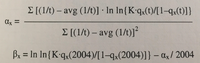

The following method is used for alpha and beta:

αx = ∑ [(1/t) – avg (1/t)] * ln ln {K*qx(t)/[1 – qx(t)]}

∑ [(1/t) – avg (1/t)]²

βx = ln ln {K * qx(2015)/[1 – qx(2015)]} – αx / 2015

and K = 10^6

I have attached a file, where I tried to simulate these numbers.

on sheat 1: my simulation for betas corresponding the above formula

on sheat 2: the mortality rates of the past on which the alpha and betas are based.

If anyone can help me simulating alpha.

For beta I already simulated (see sheat 1) and for the first three years, the calculated beta correspond with the beta. After the third year, it doesn't. Maybe there is a kind of smoothing formula which I couldn't find.

The following method is used for alpha and beta:

αx = ∑ [(1/t) – avg (1/t)] * ln ln {K*qx(t)/[1 – qx(t)]}

∑ [(1/t) – avg (1/t)]²

βx = ln ln {K * qx(2015)/[1 – qx(2015)]} – αx / 2015

and K = 10^6

I have attached a file, where I tried to simulate these numbers.

on sheat 1: my simulation for betas corresponding the above formula

on sheat 2: the mortality rates of the past on which the alpha and betas are based.

If anyone can help me simulating alpha.

For beta I already simulated (see sheat 1) and for the first three years, the calculated beta correspond with the beta. After the third year, it doesn't. Maybe there is a kind of smoothing formula which I couldn't find.