You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

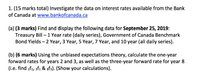

Help with Future Rates: Using unbiased expectations theory, calculate forward rates

- Thread starter MarianS

- Start date

Thank you! I thought there was another way that I was missing.You'll have to estimate it or assume it. Take your pick.

tkhunny

Elite Member

- Joined

- Apr 12, 2005

- Messages

- 11,322

Well, there MAY be. If you have not discussed it in class, and there is nothing in your text book, I see no other choice.Thank you! I thought there was another way that I was missing.

It has been literally decades since I studied this, but I think that you are ignoring that you have the current 1-year rate. If I remember correctly, we can use that to interpolate. But I hesitate to say for sure because I am unsure of your notation.

Are you denoting as [MATH]f_{a,b}[/MATH]

the imputed forward rate at the start of year a for b years or the imputed forward rate at the end of year a for b years.

Are you denoting as [MATH]f_{a,b}[/MATH]

the imputed forward rate at the start of year a for b years or the imputed forward rate at the end of year a for b years.