Timmy_Rangi

New member

- Joined

- Mar 7, 2019

- Messages

- 5

I have an exercise where I am trying to calculate a fictional property investors 'borrowing power' from the bank.

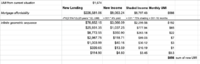

Essentially the bank calculates their income, subtracts their expenses which gives them a UMI (uncommitted monthly income).

This amount, for example, $5,000, is then tested against a 'test interest rate' of 7.3%, using a 25-year Principal & Interest Loan. Which says they can afford to borrow $688,675.54. In my spreadsheet") looks like this PV((0.073/12),(25*12),5000)

looks like this PV((0.073/12),(25*12),5000)

But. If they are purchasing an investment property, their future rental income can contribute to their UMI.

The rental income is treated specially by the bank, the bank removes 25% of it. ie If you receive $20,000 of rent, you can only use $15,000.

In addition to that, there is a limit to how much they can borrow set by their deposit and equity. I calculate this first. So for this example, let's say their equity says they can borrow $1,500,000. But obviously, they can't afford to service that much. I want to know how to find out the maximum amount that they can service.

I am assuming a 4% yield on their property investment.

In my mind there seems to be two calculations to run:

Does that make sense to you? Because it is breaking my brain!!!

Thanks so much,

Timmy.

Essentially the bank calculates their income, subtracts their expenses which gives them a UMI (uncommitted monthly income).

This amount, for example, $5,000, is then tested against a 'test interest rate' of 7.3%, using a 25-year Principal & Interest Loan. Which says they can afford to borrow $688,675.54. In my spreadsheet

looks like this PV((0.073/12),(25*12),5000)But. If they are purchasing an investment property, their future rental income can contribute to their UMI.

The rental income is treated specially by the bank, the bank removes 25% of it. ie If you receive $20,000 of rent, you can only use $15,000.

In addition to that, there is a limit to how much they can borrow set by their deposit and equity. I calculate this first. So for this example, let's say their equity says they can borrow $1,500,000. But obviously, they can't afford to service that much. I want to know how to find out the maximum amount that they can service.

I am assuming a 4% yield on their property investment.

In my mind there seems to be two calculations to run:

- the $688,675.54 * 4% yield * 75% bank discounting = $20,660.27

- then there is an amount of the equity limit of $1,500,000 that will self service?

- then the $20,660.27 means you can borrow some more, which means you can service some more.

Does that make sense to you? Because it is breaking my brain!!!

Thanks so much,

Timmy.